Market Summary: Total Addressable Market for CWS in the US Data Center Sector

As digital growth strains freshwater supplies, INFRA's Ted Douglass assesses the Corporate Water Stewardship (CWS) market.

Published on

July 15, 2026

Contributors

Ted Douglass

Sustainability Lead

.avif)

Janna Coleman

Business Operations Specialist

The Evolving Freshwater Footprint of US Data Centers

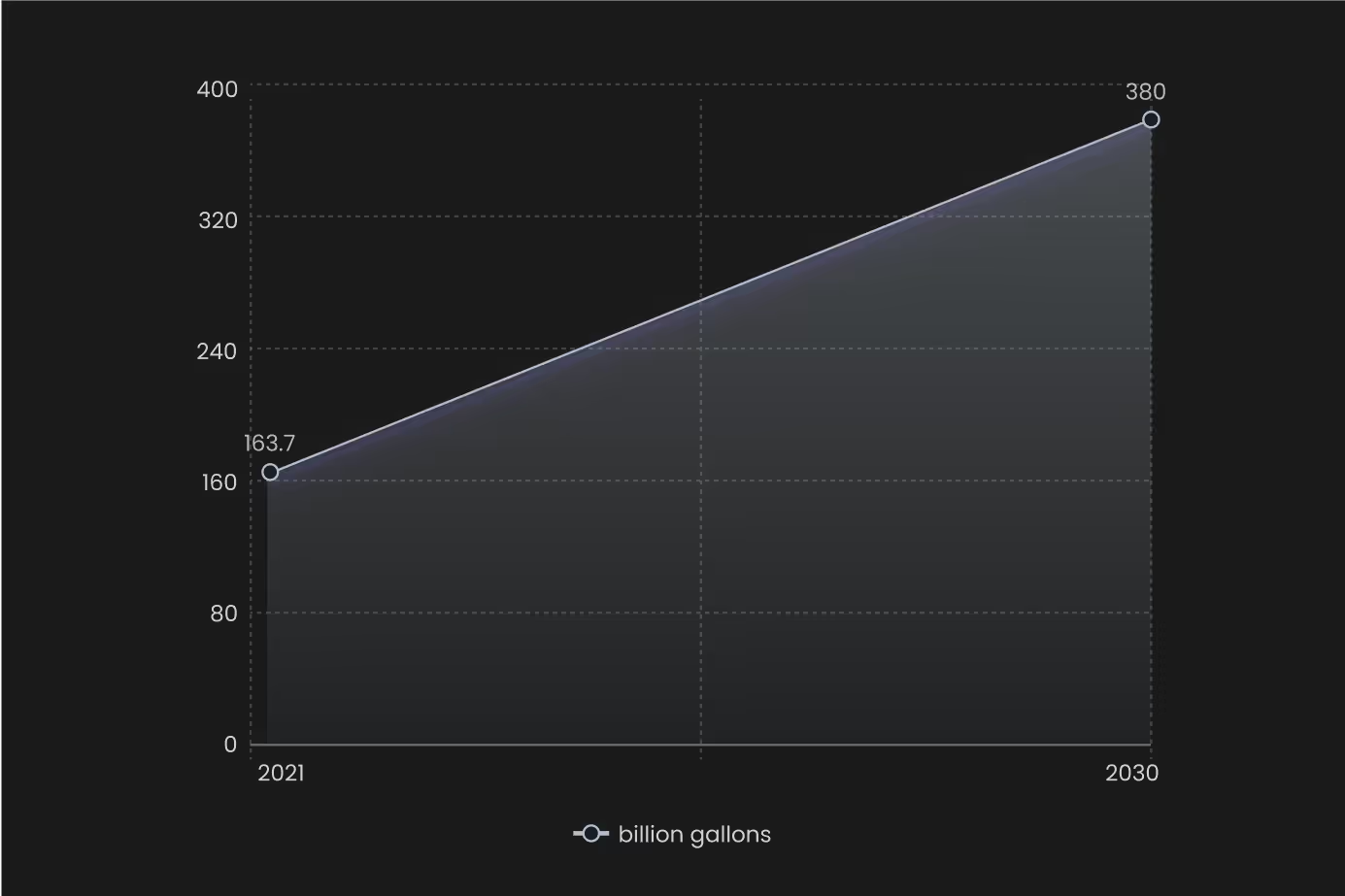

Data centers are substantial and growing consumers of freshwater, primarily for cooling. In 2021, the 5,426 data centers in the U.S. consumed an estimated 163.7 billion gallons annually.

Projections indicate a significant increase, with U.S. data center freshwater consumption expected to reach 380 billion gallons annually by 2030, representing an 8% Compound Annual Growth Rate (CAGR) from 2025.

Hyperscale data centers alone are projected to withdraw 150.4 billion gallons between 2025 and 2030. This direct consumption is further compounded by an indirect water footprint from electricity generation, estimated at approximately 211 billion gallons in 2023.

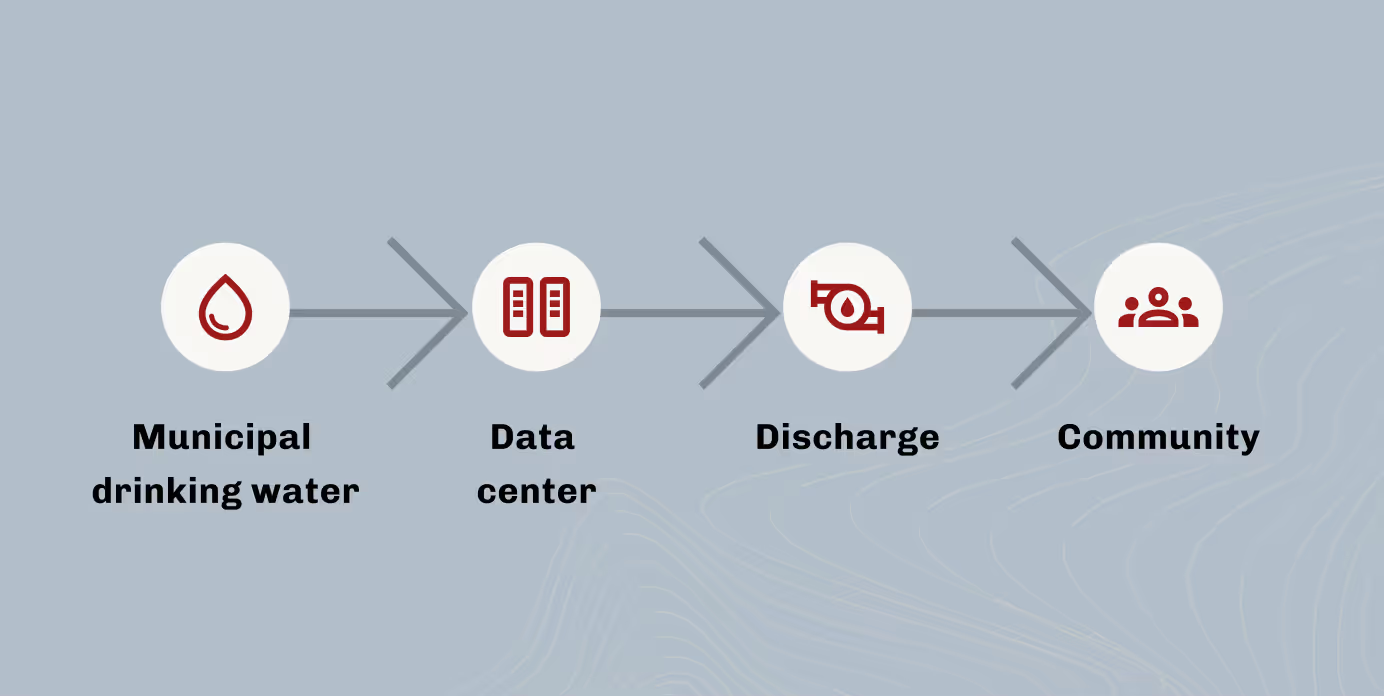

A critical aspect of this consumption is its source: over 97% of water utilized by major data center operators is drawn from municipal drinking water systems, placing direct pressure on potable supplies, often in water-stressed communities.

Data center demand is a challenge for many water managers. Due to data center demand, water draw is relatively constant with only slight variations from heat of the day to overnight low temperatures. However, normal municipal demand typically follows a diurnal curve, which has peaks and valleys with a sharp drop off in demand overnight.

The constant water demand from data centers removes some of the capability of municipal water systems to respond to acute depletion or seasonal scarcity issues.

Rapid growth in the digital economy is significantly impacting water resources, resulting in strained infrastructure, decreased water availability, and declining community relations. This underscores that Corporate Water Stewardship (CWS) must expand beyond internal operational efficiency to encompass the entire value chain and contribute to local water resilience.

Market Logic and Scope

Leading technology companies are demonstrating a profound shift in their environmental strategies by articulating ambitious "water positive" goals:

- Microsoft: Committed to being water positive globally by 2030, aiming to replenish more water than consumed through wetland restoration, impervious surface removal, and forest restoration in ~40 stressed basins.

- Google: Pledged to restore 120% of freshwater consumed globally by 2030, actively supporting 112 water stewardship projects across 68 watersheds, with a focus on agriculture-intensive areas.

- Amazon Web Services (AWS): Set a water positive goal for 2030, achieving 53% of its target by 2024. Strategies include expanding water recycling to over 120 U.S. data center locations by 2030 (conserving >530 million gallons annually).

- Meta Platforms: Committed to being water positive by 2030, targeting 200% restoration in high water stress regions and 100% in medium water stress regions. By the end of 2023, Meta had funded 32 projects in 10 watersheds, generating 1.55 billion gallons in volumetric benefits.

The consistent emphasis on "water-stressed regions" and local context for replenishment infers CWS is moving beyond offsetting a global water footprint to addressing specific hydrological and social challenges in the areas where data centers operate.

This creates a substantial demand for external water replenishment projects, particularly those that can deliver measurable benefits in water-stressed agricultural basins. The companies identified above make up roughly 65% of total water use in the US.

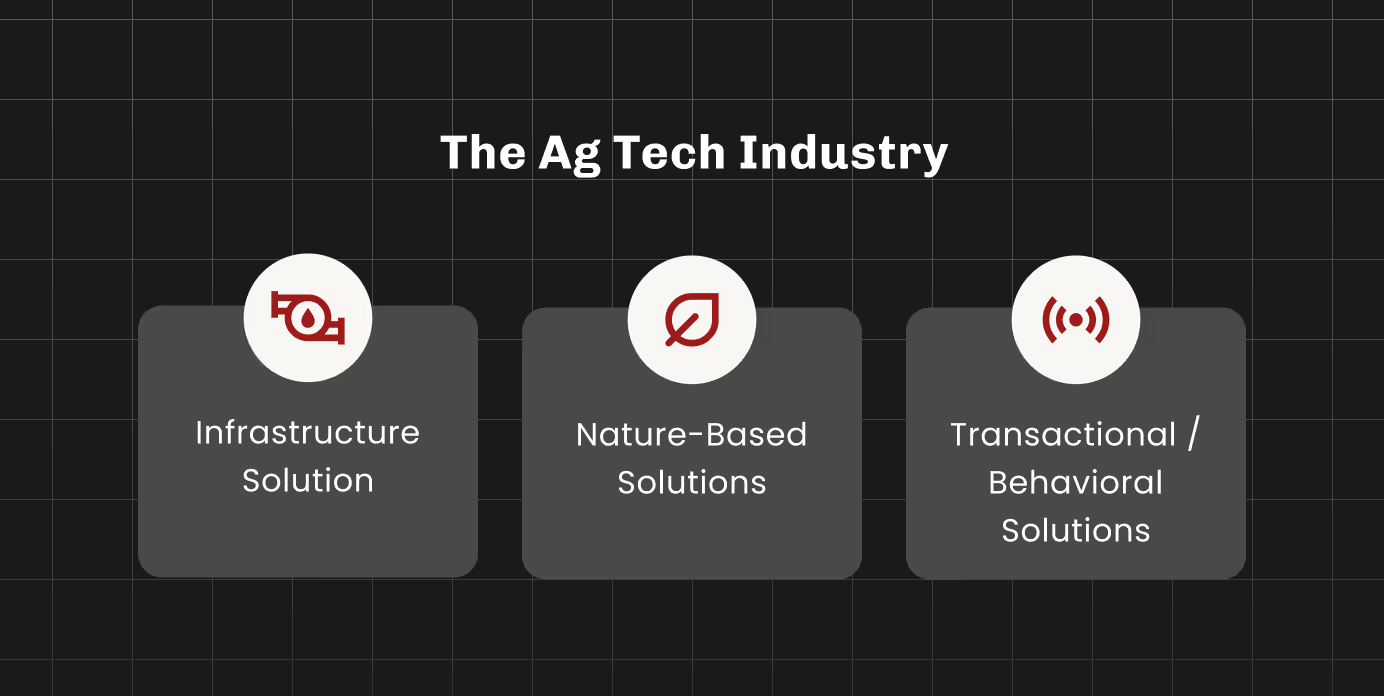

The Ag Tech Industry

The agricultural sector is the largest consumer of freshwater globally, accounting for approximately 70-80% of total usage. In the US this use is closer to 80% of all freshwater use. This positions the ag tech industry as a crucial partner for data center CWS initiatives, offering innovative and scalable solutions for water conservation.

The ag tech space can be categorized into three distinct categories: infrastructure solutions, nature based solutions, and transactional or behavioral solutions. Key water conservation technologies and practices in ag tech include:

- Infrastructure Solutions are solutions that address conveyance or distribution of water. These projects include:

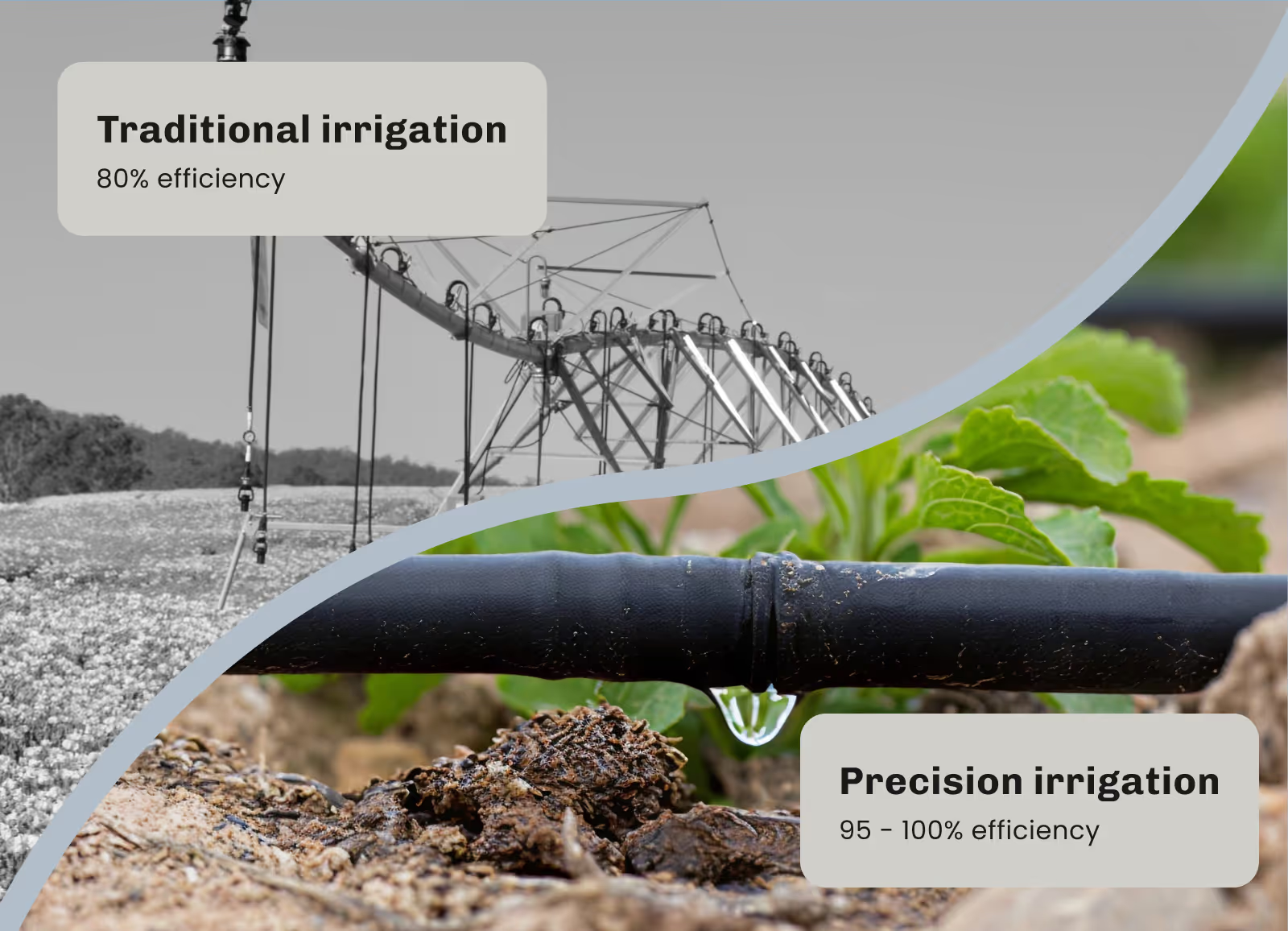

- Precision irrigation systems optimize water use by delivering the right amount of water to crops at the right time and place based on needs and environmental conditions.

- Drip irrigation delivers water directly to plant roots, achieving 95-100% water use efficiency, saving up to 80% more water than conventional methods, and often increasing crop yields.

- Water recycle and reuse technologies enable recycling and reuse of agricultural process water or treated wastewater for irrigation.

- Nature Based Solutions are often end of field solutions driven by water quality objectives. These types of projects include edge of field treatments, riparian buffers, bioreactors, and wetlands.

- Transactional or Behavioral Solutions are projects that drive efficiency practices and behaviors in water application, including:

- AI-Powered irrigation platforms that leverage AI to optimize irrigation based on real-time crop needs and environmental data, ensuring precise water application.

- Smart water management tools such as soil moisture sensors, integrated weather forecasts, and crop monitoring via drones and satellites enable informed decisions, preventing overwatering and improving resource allocation.

- Soil and land management practices include compost, mulch, cover crops, and conservation tillage that enhances soil water-holding capacity, reduces evaporation, and improves water infiltration.

Quantifiable Benefits

Water Savings: Ag tech solutions deliver significant water savings (e.g., Israel: up to 50% water reduction with 20-30% yield increase; U.S.: up to 30% reduction in some crops) while also improving crop health, reducing energy consumption, and minimizing environmental impact through reduced runoff and groundwater contamination.

This multi-faceted approach offers critical dual benefits of water conservation and enhanced food security, making it particularly attractive for CWS investments.

Cost-Effectiveness Analysis: Ag tech solutions are often highly cost-effective compared to other water stewardship alternatives.

In the Ag Tech industry, replenishment project costs per million gallons replenished/saved can range from $1,200 (e.g., ditch lining improvements) to $6,800 (e.g., precision landscape irrigation, indicative of more complex ag tech deployments).

Agricultural conservation incentives like tillage practices ($1,250/MGal) and filter strips ($3,750/MGal) also fall within this cost-effective range.

Ag tech solutions, especially those focused on agricultural conservation and infrastructure improvements, can be among the most economically attractive pathways for data center companies to achieve volumetric water benefits, offering a more efficient allocation of CWS funds.

Total Addressable Market for Data Center CWS in Ag Tech (through 2030)

The total addressable market for data center CWS funding specifically directed towards ag tech companies is a function of the data centers' escalating water footprint and their ambitious replenishment commitments.

Methodology for TAM Calculation:

- Projected Data Center Water Consumption (2030): US data centers are projected to consume 380 billion gallons annually by 2030.

- Replenishment Target: Assuming a conservative 100% replenishment target, data centers aim to return at least 380 billion gallons annually.

- CWS Commitments: Google, Microsoft, Meta, and AWS have all made commitments that include 100% replenishment of water used as part of operations. These companies make up 65% of the US Market for Data Center Water Use. Applying a conservative approach that these organizations may be the biggest investors in CWS in the Data Center space sets a 2030 target of 247 billion gallons.

- Ag Tech's Share of Replenishment: 80% of freshwater use in the US is for agriculture practices. Focused effort in this system has the highest opportunity for meaningful water replenishment. For market sizing purposes, if 50% of the data center replenishment target is directed towards ag tech solutions, this represents a 2030 target replenishment volume of 123.5 billion gallons via ag tech.

- Conversion to Market Value: Using a conservative mid-range average cost of $3,000 per million gallons for ag tech solutions.

Total Addressable Market for Data Center CWS in Ag Tech

- TAM = 123.5 billion gallons/year x ($3,000 / 1,000,000 gallons) = $370.5 million of investment between today and 2030.

Strategic Insights

The data center industry is highly competitive and real budgets and approaches are closely held and confidential. Very few programs are presenting investment amounts with volumes replenished.

The investments in this space have grown exponentially over the last 2-3 years. However, it is difficult to leverage the publicly available data to determine actual program budgets for 2030 targets without published investment amounts.

The estimates provided in this summary are conservative, as it only considers direct data center consumption and a 50% allocation to ag tech. If indirect water consumption, higher replenishment targets (e.g., 120% or 200%), or a higher average cost for more advanced ag tech solutions are factored in, the TAM could be significantly larger.

We have seen a 50% increase in cost over the last 5 years in project costs. It is likely that the increase in demand and the preference for high quality projects have driven up the average cost per million gallons replenished.

The limiting factor in this market is demand, which is outpacing supply. Some industry professionals have identified that the current supply pipeline does not have the capacity to provide enough projects that meet the quality and delivery of replenishment projects to the CWS commitments being made.

"Demand for high-quality replenishment projects is outpacing supply."

The speed and scope of innovation in data center delivery technology is rapidly evolving. The Deepseek breakthroughs, identified in January of this year, hinted at evolving adjustments in water use expectations to deliver AI at scale.

Innovation is outpacing delivery but will take some time to influence the overall infrastructure build in the US. It is a conservative assumption that disruption in the building of US data center infrastructure is on the horizon but may not be meaningful before the realization of the 2030 commitments.